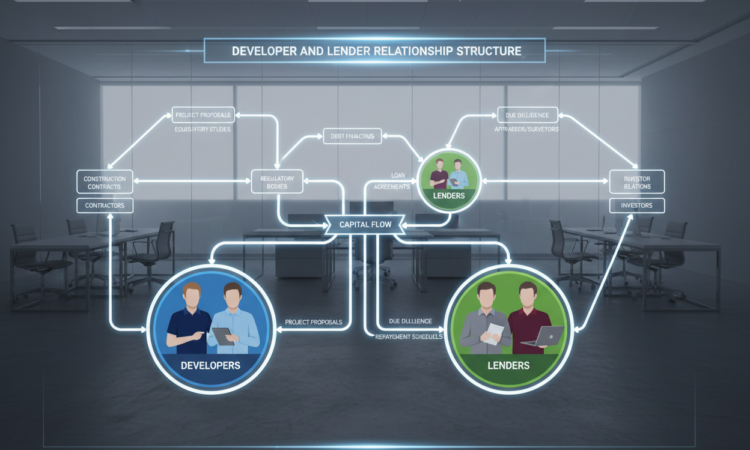

Developer and Lender Relationship Structure

Successful real estate development in Costa Rica hinges on a strong partnership. This is especially true for private, asset-backed lending. The right relationship between a developer and their capital source is the foundation of any project.

We focus on a conservative, security-first approach. In plain English, this means we prioritize first-lien mortgages. This structure gives the lender a secure position, backed by the physical property.

Our team brings the necessary expertise to navigate this market. We’ve managed complex projects—like Spiller Builders’ Bristol development with 13 Party Wall Agreements. Director Anil Bains oversaw the construction of five new homes in Chesham. This hands-on experience is crucial.

We understand every developer has unique needs and timelines. Our goal is to provide stable funding and clear communication. This creates a professional environment where construction finance works for everyone involved.

Understanding the Developer and Lender Relationship Structure

engage in a focused discussion around a modern conference table. In the middle ground, a large window showcases a lush tropical landscape, emphasizing Costa Rica's natural beauty. The background features contemporary office elements like potted plants and abstract artwork on the walls. Soft, warm lighting creates an inviting atmosphere, highlighting the professional yet approachable mood, while maintaining a sense of collaboration and trust between the lender and developer. The angle of the scene is slightly elevated, giving a broad perspective on the interaction and environment.")

Navigating property development here requires more than capital. It demands an aligned vision between the funding source and the builder. A structured, conservative partnership is the best way to manage risk and ensure success.

Key Elements of a Conservative Partnership

Trust is built through transparency and clear documentation. We use tools like Rabbet software to organize loan files. This reduces errors and speeds up the financing process.

Open communication keeps both parties aligned on project goals. We focus on long-term relationship development, not just single transactions. This approach, similar to funds like Fidelis, often leads to better terms for repeat borrowers.

Tailoring Your Approach for Costa Rica

The local market has unique needs. A deep understanding of registry systems is non-negotiable for proper property vetting. Our team has this specific experience.

We provide the information you need to make informed decisions. This helps navigate land acquisition and construction completion. Establishing a solid track record with us can lead to faster approval times for future projects.

Core Structure: Emphasizing First-Lien Mortgages

The core of our lending framework is built on two non-negotiable principles: first-lien security and conservative loan-to-value ratios. This structure directly protects the capital we provide for your construction project.

In plain English, we only act as the primary mortgage holder. This gives us, and by extension our investors, the strongest possible legal claim to the property if anything goes wrong.

Prioritizing Safety with No Second Lien Policy

We strictly enforce a first-lien only policy. We never participate in second liens or subordinate our position. This eliminates complex risk layers and ensures clear collateral recovery.

Our approval process includes verifying the borrower’s equity stake. This proves they have significant skin in the game, aligning their commitment with the project’s success.

Maximizing Protection with a 50% LTV Guideline

Our standard is a 50% loan-to-value (LTV) guideline. This means we typically finance only half of a property’s appraised value.

This creates a large equity buffer. It protects against market shifts and ensures the developer’s commitment remains high throughout the construction period.

Final funding often requires a Certificate of Occupancy. This confirms the building is habitable and meets all codes, securing the loan’s collateral.

Risk Controls and Conservative Underwriting

To protect both the project and the capital, we enforce strict verification and documentation protocols. Our underwriting process is designed to identify and mitigate potential issues before funding begins. This creates a secure foundation for every real estate development deal.

Implementing Borrower Verification and KYC Basics

We start with strict KYC (Know Your Customer) basics. This means verifying the identity and financial background of every borrower. We analyze financial statements, tax returns, and insurance deposits. This review confirms the borrower’s ability to complete the proposed building project.

Maintaining Clear, Written Terms and Proper Documentation

Clear, written agreements protect all parties involved. Proper documentation of change orders and invoices is critical. It prevents project delays and ensures smooth draw request approvals. This transparency minimizes miscommunication and keeps the construction finance process accountable.

Ensuring Collateral Security and Title Verification

Before any capital is committed, a thorough verification of the property’s legal standing is non-negotiable. This step protects the lender’s interest and the developer’s project from future disputes.

Conducting Clean Title and Registry Checks

We conduct rigorous clean title and registry checks in Costa Rica. Our goal is to confirm the property is free of undisclosed legal encumbrances.

We verify that all parties have the necessary legal standing for a binding financing agreement. This ensures clear access and building rights for the developer.

Reviewing Encumbrance, Valuation, and Equity

A development appraisal is a standard requirement. It determines the site’s value before approving any construction financing.

Our valuation process involves a detailed review of the property’s equity. This ensures the loan stays within our conservative 50% LTV limit.

Lien waivers are essential documents we review before approving a draw request. This thorough collateral summary provides peace of mind for our clients.

It creates a solid foundation for a secure lending relationship on every deal.

Focused Controls for a Solid Lending Framework

Specialized lenders earn higher returns by expertly managing the unique risks of the construction phase. This expertise demands a disciplined framework. We use automated systems to flag inconsistencies, making our evaluation faster and more accurate.

Establishing Conservative Underwriting Practices

Conservative underwriting is the cornerstone of our framework. We analyze the borrower’s financial health and project track record. This ensures they have the capability to complete the development as planned.

This structured evaluation protects all parties. It creates a stable environment for the project and the lender. A solid framework is essential for long-term success here.

Our commitment means we only fund demonstrably viable projects with strong collateral. We provide the expertise to navigate complex construction financing. Our focus on clear, written terms ensures everyone is aligned.

Best Practices in Documentation and Closing Procedures

We treat the closing process as a critical checkpoint. It verifies all project requirements are met before final funds are released. This meticulous phase protects everyone’s interest and ensures a smooth transition to project completion.

Performing Detailed Collateral Summaries

For every deal, we perform a detailed collateral summary. This document clearly defines the lender’s security position. It is legally reviewed to ensure maximum protection.

The final draw request is a key part of this. It requires confirmation from all parties that the development meets local codes. This step confirms the property is truly ready for occupancy.

Ensuring Proper Closing and Lien Registration

Our closing procedures are efficient and transparent. We verify every lien waiver and conduct a final property inspection. This ensures the construction is habitable and meets our standards.

We work closely with local legal experts. They ensure every lien is registered correctly in Costa Rica’s system. This provides maximum security for the lender and confidence for our clients.

This careful process minimizes final-stage risk. It secures the loan and supports a successful project completion. Our experience allows us to handle even complex closings with accuracy.

developer-lender-relationship-structure in Practice

Clear communication and structured reviews form the operational backbone of every successful development deal. Our framework moves from theory to action here. It ensures both the lender’s security and the developer’s vision are protected throughout the construction phase.

Structured Risk Mitigation and Clear Loan Terms

We believe unambiguous loan terms are essential. They provide a concrete roadmap for the entire project lifecycle. This clarity mitigates risk by aligning expectations from day one.

Our terms detail draw schedules, inspection points, and completion milestones. This structured approach prevents misunderstandings. It keeps the financing process smooth and predictable for all parties involved.

Ongoing Monitoring and Conservative Risk Reviews

Active monitoring is not optional; it’s a core part of our service. We conduct regular site visits and financial reviews. This allows us to identify potential issues early, alongside the developer.

These conservative risk reviews are proactive. They help us address challenges before they impact the project’s timeline or budget. This ongoing diligence protects the lender’s interest and supports the developer’s track record.

This hands-on partnership, built on transparency, is what turns a good deal into a great long-term relationship.

Partner with GAP Investments for Secure Funding Solutions

Your next development venture deserves a financing process built on security and clarity. We provide that foundation. Our team brings direct experience to every project, focusing on conservative risk controls that protect your capital.

Ready to move forward? Contact our expert team to discuss your specific property and construction needs. Reach us on WhatsApp at +506 4001-6413 or call our USA/Canada line at 855-562-6427.

Visit gapinvestments.com to learn more about our approach. Please note, this information is for educational purposes and does not constitute a financing offer. We build lasting client relationships on transparency and a proven track record.

FAQ

What makes a developer-lender relationship structure secure?

A secure structure is built on transparency and aligned incentives. We prioritize first-lien mortgages, enforce conservative loan-to-value ratios, and conduct rigorous due diligence on every project and borrower. This approach protects all parties by ensuring the collateral is solid and the deal terms are clear from day one.

How do you protect my investment as a lender?

Our primary protection is through a strict, no-second-lien policy and a maximum 50% loan-to-value guideline. This creates a significant equity cushion in the property. We then layer on verified borrower credentials, legally registered liens, and precise documentation. We manage this process so you have a clean, enforceable claim on valuable collateral.

Why is the loan-to-value (LTV) ratio so important in Costa Rica?

In any market, but especially here, a conservative LTV is your first defense against risk. By capping our loans at 50% of a property’s appraised value, we ensure there’s substantial borrower equity at stake. This dramatically reduces the chance of default and protects your capital if we ever need to execute on the collateral.

What does your underwriting process involve?

Our underwriting is a deep-dive into both the person and the project. We verify the borrower’s background and financial capacity—know-your-client basics. We then scrutinize the property’s title, valuation, and any existing encumbrances. Every requirement and term is documented in writing before funding, leaving no room for ambiguity.

How do you handle property titles and legal registration?

We perform a thorough title search at the National Registry to confirm clean, marketable ownership. Before any funds are released, our legal team ensures the mortgage lien is properly drafted and registered against the property. This legal step is non-negotiable; it’s what formally secures your position as the lender.

What happens during the loan closing process?

Closing is where our structured approach culminates. We prepare a detailed collateral summary, coordinate with a trusted escrow agent, and ensure all funds are disbursed against verified milestones. The key moment is the official registration of the mortgage, which we handle directly. You receive a complete dossier of the executed, legal loan documents.

Do you monitor the loan after it’s funded?

Yes, proactive monitoring is part of our service. We track payment compliance and stay informed on the project’s progress or the property’s status. Our team conducts periodic reviews, and we communicate openly with the borrower to address any issues early. This ongoing oversight helps prevent small problems from becoming major risks.

Why should I work with GAP Investments for this type of financing?

We simplify a complex process. For foreign lenders and expats, navigating Costa Rica’s real estate and legal systems alone is challenging. We act as your expert guide and process manager. We apply a conservative, transparent framework to every deal, focusing on securing your capital with clean collateral. You get a pragmatic partner, not just a loan broker.

Article by Glenn Tellier (Founder of CRIE and Grupo Gap)